Read as PDF…

I am in my 50ies now, and obviously I read and have read a lot of books. I was late to find interesting things about investing, on Twitter and online in general. But these days I find more and more very high-quality material online, and also a genuine desire to share and educate. As most things online, I stumbled across Ensemble Capital a few years ago, and was immediately struck by the quality of what they produce, and in so many ways and forms. A great blog, twitter & quarterly calls, with detailed discussion on what went wrong and what went right. Regardless if you agree or not with their conclusions, you should learn more about their ideas and their processes. Below you will get a jumpstart, thanks to Arif.

Out of the blue I just sent Ensemble an e-mail, which Arif picked up, and he kindly agreed to answer some very detailed questions. Not many would take the time or be able to answer in this fashion. He shares details about his personal journey in the investing world, which I think are highly inspirational. You are all in for a treat. Enjoy! /Bo

Arif is a senior investment analyst at Ensemble Capital. Before joining Ensemble Capital, he was a senior investment analyst and co-portfolio manager at Kilimanjaro Capital. Positions prior to that included senior equity analyst at Pacific Edge Investment Management and research associate at Robertson Stephens & Co. Arif graduated from the Massachusetts Institute of Technology with a BS in Economics and he is also a CFA charterholder. Follow Ensemble here: https://twitter.com/intrinsicinv or here: https://ensemblecapital.com/.

Dear Arif, Thanks for the Q&A opportunity. You, and your firm, is an example of how sharing increases everyone’s knowledge, both your own, your readers and your investors. I am very impressed with the content on your site. So, let's get started.

1. Please tell us something on how you personally found your investment style, and what experiences have formed your investment beliefs over time. If you mention a book or two, we would appreciate it.

First of all, thank you for your kind words and this opportunity to speak with you and all your readers, Bo. We write about and discuss our ideas both to share our perspective based on our experiences and to connect with those with similar investment philosophies, so we can learn from them as well and continue to evolve our collective investment acumen.

As far as my own evolution as an investor, I stumbled into investing after my 10thgrade math teacher roped me into a new investment club she started for a local newspaper competition. That got me hooked on investing and business. Later in college, I read Peter Lynch’s Beating the Streetand it suddenly dawned on me that I could be an investor for a living, which literally felt like an epiphany since I loved my investing side hobby! I had also heard about Buffett as this great genius investor but didn’t really get to reading his writing till after college (I tried to tackle The Intelligent Investor, but it was too dry and unrelatable).

I moved to the San Francisco Bay Area, both because it was the hotbed of technology and also because I learned Wall Street just took itself too seriously after interning there. I loved the attitude in San Francisco, where people took pride in both working hard but also playing hard in its active, beautiful natural environment – it seemed a lot more of a balanced focus and it was just my style!

I worked at an investment bank in the middle of the Dotcom boom, while I was reading about Buffett – his sensibility and investing style just made sense to me. I think people are drawn to investing styles that resonate with their personalities and value investing certainly suited mine.

But it was hard to be a value investor at a sell-side research department that pitched technology companies that were very highly valued, justified by very optimistic growth prospects, eyeball metrics, and “GIGO” DCF calculations. While the thematic “thought pieces” discussing grand future did turn out to be generally prescient, the business models would take a decade or two to come to fruition, with most of those early companies sidelined to irrelevance. However, a few of those that survived the cold winter of the Dotcom Bust grew to become vastly more valuable than anyone would have imagined (e.g. Amazon, Booking Holdings).

I knew I wanted to end up on the buyside like my favorite investors at the time, namely Peter Lynch, Warren Buffett, Bill Miller, and George Soros, but I also loved technology… so I was fortunate to be introduced to a wonderful woman who managed a small cap long/short value tech fund, and we just hit it off. She ticked all my boxes – smart, a genuinely nice person, with a long/short value investment style that resonated with me. And I had a great experience working with her, where she taught me the ropes of investing in small/mid cap tech. It was an especially exciting time when I joined her in 2000… shorting stocks was really fun then!

But by 2007, I felt like the sandbox we were investing in was getting to be too limiting and my interests had grown beyond tech. In addition, small cap tech investing was mostly about taking advantage of near-term product cycles and I wanted to be able to invest in higher “quality” companies that could sustainably grow (“compound”) profitably over long periods of time. It was a sort of coming of age moment for me.

I took a year off to travel in 2008 to see the world with my wife, a “bucket list” dream we both shared, and came away with an understanding that I had naively never thought about – countries around the world were developing and people all pretty much had similar desires and goals underneath their varied cultures. It just opened the world to me as a human and an investor.

In addition, I saw the potential of the iPhone and internet connectivity as a power user during my travels. I could do everything with it – take pictures, listen to music, email, call, make hotel and flight bookings. It was a computer in my pocket, and I was able to connect to the internet from the mountains in the Andes to beaches in Thailand and in every major city in the world. It was an incredible realization! And I was convinced that the wealthiest 20% of the world’s population would want one and be willing to pay for one.

My travels brought that insight of global connectivity, applicability of key preferences across geographies, and the global scale certain types of businesses could achieve.

When I returned in 2009, I started my own investment fund - I had lived in Silicon Valley and, of course, I wanted to try my hand at my own startup! As an investor, I wanted to learn and morph into a generalist, who sought out companies with secular global growth tailwinds and competitively advantaged business models. There was a steep learning curve involved in running a business for the first time, in learning about industries outside of technology, and in managing a portfolio. My partner and I had a lot of fun and learned a ton on how operating businesses actually work and how value creation works in the real world.

Ensemble Capital Management reached out to me at the right time in 2015, when I was ready to go from a multifaceted role of running and trying to scale my own business back to focusing on investment research on companies, which is my true passion. As I learned more about the firm, I realized Ensemble was the “grown up” version of the firm I had been trying to build, with the right complementary investment philosophy (concentrated portfolio full of “moaty” companies), a disciplined strategy focused on business analysis (it takes conviction and courage to truly be a long term investor), and yet it had the flexibility to evolve its process with new learnings. In Sean Stannard-Stockton, the President and CIO of Ensemble, I found a kindred investor who is also curious, open-minded, and grounded in good judgement. Along with Todd Wenning, we’ve enjoyed working together, uncovering new companies, and continually improving our investment process and acumen.

In summary, my natural inclination towards value investing combined with my intellectual interest in investing, technology, and business value creation led me through a series of learnings that took me from the traditional mold of a value investor of the deep-value Ben Graham cigar-butt style backward-looking investor to a quality, moat-oriented, forward-looking intrinsic value investor.

As far as books are concerned, I read a lot of different types of books, usually in waves of thematic interest. Some of my favorites related to investing and business are popular/biographical reads like Roger Lowenstein’s and Alice Schroeder’s biographies of Warren Buffett, Peter Kaufman’s Poor Charlie’s Almanack, Damn Right by Janet Lowe, Brad Stone’s The Everything Store, Mark Robichaux’s The Cable Cowboy, Ray Dalio’s Principles, and Jim Collin’s Good to Great and Built to Last. I also like broader concept/history books like Michael Mauboussin’s More Than You Know, Yuval Harrari’s Sapiens, Jared Diamond’s Guns, Germs, and Steel, and Peter Bernstein’s Against the Gods.

A couple of influential books outside of business for me were the science fiction book Stranger in a Strange Land by Robert Heinlein, which opened up my view on frame of reference in many ways, and Robert Pirsig’s Zen and the Art of Motorcycle Maintenance, which got me thinking more philosophically on the intersection of my life and my career around personal long term goals.

2. As the core of Ensemble's process you mention that you have “the same essential approach used by many of the truly great investors over the last century” Anyone you would like to mention? Some books you can mention that everyone can learn from.

The obvious one for any value investors are Warren Buffett and Charlie Munger. And there are simple lessons that people have traditionally taken from Buffett on value investing. However, anyone who also is familiar with Buffett’s history also appreciates how flexible he has been over time in adapting his approach from cigar-butt investing in his early partnership learned from Ben Graham, his early mentor, to moat-oriented quality investing from Munger, to most recently stating how Apple, Microsoft, Amazon, Google and Facebook are “ideal businesses” in 2017– that from an investor that traditionally eschewed technology companies because they were hard to value.

And mind you, I don’t think it’s that he was unable to understand the companies necessarily, but he couldn’t foresee the probabilistic range of outcomes 10-20 years into the future in any comprehensible way that could enable him to assess their intrinsic business values. Because technology changes so fast and companies leap frog one another regularly, they have traditionally been unforecastable. Over time that has changed with certain companies demonstrating network effects, user switching costs, and brand power.

The common thread in all this is that Buffett’s investing success relied on owning competitively-protected, high return on capital businesses over long periods of time for which he could reliably forecast future cash flows. What that business looked like evolved over time and Buffett has too, even in his 9thdecade. It’s no wonder that he’s been so successful an investor over a lifetime!

Then of course there are other investors that we admire that have similar fundamentally based approaches to being patient long term investors in competitively advantaged companies like Chuck Akre, Bill Nygren, and Tom Gayner.

The books mentioned above are great references to these lessons. I’d add to the list 7 Powers by Hamilton Helmer as an interesting lesser known book on frameworks to building moats.

3. You write that it’s easy to understand your approach but difficult to execute. Why is it difficult to execute, please provide some further color?

We think there are two distinct reasons why our investment approach is difficult to execute – one is temperament and the other is identifying the character and relevance of moats.

It difficult to execute because there is a temperament required to be able to own shares in companies that exhibit strong competitive advantages when they are down and out, sometimes over long periods of time. It requires you own the company when there are many doubters, both intelligent investors in the market and media reports bombarding you on why the business is broken or obsolete or will face terrible times ahead because of recession, competition - you name it.

On the other end it’s hard psychologically to become a new or larger owner of a company whose shares have appreciated a lot over a year or five and exhibits what looks like a full valuation based on superficial shortcuts like P/E ratios. Additionally, it’s hard to sell the great businesses you love owning in your portfolio when their valuations become significantly extended beyond the optimistic end of your realistic probabilistic scenarios.

Also, identifying the character and relevance of moats is a very dynamic, subjective, and qualitative thing. While traditional moats have been thought of as sort of static characteristics of companies such as brands, scale, etc., there are many others that don’t fit well into these well established buckets, while some companies with these well-established moats have also seen the relevance of their moats declines. What is now becoming a common example are companies like Procter and Gamble, whose brand and marketing scale advantages have diminished because of social media and e-commerce, while cultural changes are impacting the relevance of Coca Cola’s core product portfolio. Examples of companies we own that don’t fit neatly into traditional moat analysis are First Republic Bank and Netflix.

So, our approach is really about identifying companies that could have strong moats, then doing the fundamental work to understand the nature and dynamics of the moat and the business model and how it creates value for customers and other stakeholders. And then using that fundamental work to build a model that can inform our valuation framework based on future cash flow generation that incorporates a range of realistic scenarios to derive a value for the business. Finally, it’s about having the guts to trust your research, analysis, and framework to filter out the noise outside of the fundamentals that inform your conviction and valuation. All of that is very hard to execute on in our experience and requires a lot of discipline.

You also have to be flexible enough mentally so that when the facts change, as to either the strength of the competitive advantage or the growth characteristics of a business, you have the wherewithal to adjust your perspective of a company you owned, regardless of it being a big winner or loser to date. You have to have the conviction and discipline to do the appropriate thing on a go forward basis, whether it be to cut the position or buy more based on the changing fundamental factors.

Filtering the noise from the signal, without ignoring the signal, is one of the biggest challenges that we all face in mitigating our natural biases.

The collection of all this is often seen as the guts to be contrarian and stubborn in buying cheap stocks. However, the opposite also applies when recognizing the market is right on seemingly high valuation stocks at times, and even not enthusiastic enough in certain situations. Classic examples of these would be companies like Google, Mastercard, or Broadridge… all stocks that have outperformed the market over long periods of time because the market was not enthusiastic enough for many years, even during times when they appeared to be “richly valued” on an absolute, relative, or historical P/E basis.

4.You are in short “business analysts” where you are buying the stocks of these great companies when they are priced at a discount to their intrinsic value. Why do you think that disconnect exists?

The biggest disconnect is the short-term orientation that exists in a lot of the market as far as inputs into valuation for companies based on near term results. It’s hard to stay focused on the character and strength of businesses in the face of near-term headwinds to their financials – in other words this is “Mr. Market”. There are all sorts of incentives that cause many investors to focus within a 6-12 month window for garnering returns, a time horizon when the bulk of stock price performance is based on sentiment changes vs fundamental changes in value that manifest over longer time horizons.

In addition, we’ve written about the market’s focus on growth, which is a fleeting characteristic generally for most companies, instead of return on capital, which is a much more durable characteristic when combined with competitive advantage. Our focus on the latter, and our long term 10-year investment horizon, gives us a better perspective, in our opinion, as to what is an investable business for us and its true intrinsic value. And we can be patient enough to let those results play out (“In the short run, the market is a voting machine but in the long run, it is a weighing machine”). Our experience investing in high quality, moaty companiesso far has generally proven this to be true.

Don’t get us wrong though – we do think that the market is generally right (i.e. efficient) in the way it values high quality business most of the time. So, we have to be patient and on the lookout for those that we are interested in to fall out of favor for temporary reasons and take advantage of those opportunities or find those companies where the market is not enthusiastic enough at current valuations.

5. You often emphasize the importance for a company to have strong barriers to entry, or wide moats. Can you present some typical signs of moat erosion and how to identify it before it’s already reflected in the price? And how about widening the moat? How much do you sweat on the competitors and the risk that they may improve even faster?

This is a great question, and it’s a challenge to be honest. It’s generally a qualitative thing evaluating the strength of moats to conclude that it is eroding or strengthening. We are focused business investors, so we begin our research process trying to evaluate if a moat exists in any business we’re interested in. That moat is always forefront in our minds as we study and follow businesses over time.

Since we are business analysts and we run a concentrated portfolio, we gain a lot of knowledge about the companies we own, their industries, value chains, and competition. We often internally debate significant actions or strategies they employ, to understand the impact those have on the quality of their moats and the impact to their long term business and financial models, positive or negative. The fact that we all share the same investment philosophy in our research team and share a similar vocabulary helps us shape the framework within which we have these debates.

There’s a huge challenge in identifying the tipping point when we admit that a company’s moat is weakening because some signals can be transitory. For example, the narrative that Apple’s iPhone is “losing” market share between product cycles when everyone is screaming “Apple can’t innovate” only to then rave about the next great new product no one can live without followed by new revenue and profit records.

Contrast this with more permanent signals, like watching the trend at Pepsi, where for a number of years its revenue growth was driven primarily by price increases with flat volumes, i.e. its brands losing relevance to new competitors who were the drivers of incremental market volumes. We deemed Pepsi’s challenges as more permanent, which is why we decided to exit that position after owning it for a several years.

Surprisingly, it’s similar the other way, where one of the members of our team will start to believe that a company’s moat(s) has actually improved, and we need to reevaluate our assumptions behind valuing it (to the upside). The rest of the team members will also need to be convinced that it’s a true permanent change in moat dynamics, which is not always easy either!

An example of this was Schwab, where our conviction in the moat improved even as the fees on its large AUM business were forecasted to permanently decline towards zero. This seems counterintuitive until one realizes that the AUM fees are both leverageable with scale and are the key decision factor for customers’ competitive evaluations, while its Bank business is the true go forward monetization platform. So, Schwab’s market share and scale grows as customers choose it for the lowexplicit costsacross 85-90% of their assets (and great client service too), while Schwab makes it money on its Bank’s net interest margins (NIM) earned on customers’ cash balances, an implicit opportunity cost to them. This created a unique model that created more overall value for the customer and increased Schwab’s scalability than we had previously understood. You can find more details about our Schwab thesis in our Ensemble Fund letter here.

My colleagues Todd Wenning wrote about the weakening moats in a couple of recent posts here and here, while Sean has discussed the weakening of CPG brands here and here for a deeper discussion on the topic.

6.Investing is all about expectations. The companies you focus on is therefore 1. Exceptional franchises, but importantly also 2. Where the market forecast a quicker regression to the mean. How much of your time do you spend on analyzing the companies that you deem to be too pricy at the moment but that you would like to own at the right price, compared to existing holdings and potential new companies?

There’s some balance that happens as a result of opportunity and luck. As we’ve discussed, it’s hard to really know beforehand what the outcome of our valuation analysis will be vis a vis the market price that a company’s stock is trading at until we’ve done our own fundamental work. So, there are some years where our work is more immediately fruitful and leads to greater numbers of companies being included in the portfolio, and others where it’s not as much. And of course, there are some portfolios of companies that have a lot more dynamism in their businesses and others that are more stable for extended periods of time where there really isn’t much changing beyond just tracking the execution of the company. So there’s not a great answer for this question, it just varies from year to year depending on opportunities and existing portfolio company dynamics.

7. A key metric for you is ROIC, and you focus on companies that generate high or improving ROIC, as those businesses, all else equal, deliver the greatest shareholder value (your statement).

a. That’s fine, but what valuation metric do you look at?

We do detailed research and modeling of a business to understand both the level of profitability/growth it can achieve compared to historical base rates and the amount of it is likely to consume in order to grow and sustain its moat. That drives a long-term ROIC that then drives what the fair value multiple should be as an output. This can be restated as we have a diligent DCF methodology that gets us to a value for the business that captures the range of future probabilistic outcomes, which is what we rely upon to make portfolio execution decisions. But we don’t use the short hand valuation metrics commonly talked about in the market like P/E, EBITDA, or book value multiples, though our detailed analysis and cashflow forecasting work will spit out these multiples obviously that we can compare to history.

But you must keep them in perspective – these multiples reflect the underlying cashflow economics of the businesses, so if ROIC is improving over time or capital intensity is declining, the multiples will deservedly track higher and vice versa. So it’s important to do the modeling work informed by all the qualitative work done to understand business characteristics over time to get a truly informed view of its intrinsic value.

b. When does something become too expensive, or does it?

When the stock price materially surpasses what we’d want to get paid to sell the business if we owned it entirely, i.e. 20% premium over our fair value estimate in our case.

c. How important is the direction & pace of the direction of the ROIC? Maybe you can share an example.

The direction is important but not the end all and be all because again, you must be careful to decipher transitory or cyclical changes vs permanent changes. We don’t pay a lot of attention to the pace so much as the underlying fundamental factors affecting the direction in comparison to our forecasts based on our understanding of the business.

Ferrari is a great example, where our initial investment relied on the insight that the company had a stronger underlying ROIC potential than historical financial statement analysis indicated, while our continuing investment in the company looks through the depressed ROIC the company will see over the next couple of years of heavy investment in powertrain electrification and model expansion before normalizing at very high long-term rates. For more details on our Ferrari thesis, please see our post here.

8. What is a substantial discount to your estimate of the intrinsic value? Related to this, how do you work with the target over time, i.e. how to handle positive/negative deviations over time? In my view the main risks are holding on to companies getting weaker, and selling great companies getting stronger, vs the initial thesis.

A substantial discount for us is at least a 20% discount from our estimate of a company’s intrinsic value, which generally incorporates a few layers of conservatism. Of course, we’d like to buy companies at even greater discounts to fair value, but a minimum 20% discount to the current intrinsic value translates to a 25% upside from the current price. So if it takes 5 years to close the price gap to intrinsic value (assuming we’re roughly right in our estimate), then the stock will outperform by 4-5% per year over those 5 years.

We then have a sliding scale as that discount widens or contracts in terms of portfolio weight for a particular position relative to others in the portfolio. We cross that to a qualitative conviction scoring framework, which informs the boundaries and pace position size based on our ranking of specific qualities related to the moat, management team, our ability to understand and forecast the business, etc. So, our position sizing is comprised of a matrix that incorporates both quality in terms of our conviction framework and a quantitative discount to our intrinsic value estimate.

Improving/deteriorating qualitative fundamentals will show up in our conviction scoring while improving/deteriorating financial performance will show up in our financial model. The qualitative and quantitative are also interrelated because they inform each other in our forward-looking forecasts, and therefore impact our overall intrinsic value and weight of the position in the portfolio.

9. You mention that there are two key elements of successful portfolio management that are not practiced by the majority of investors. Less diversification & diversify within the client’s portfolio. If we start with the former. Totally agree…but how to choose between and size the best ideas? Mechanic rules on distance to target, adjust for volatility or subjective risk measurement. Rebalance, i.e. increase in loser, sell winners.

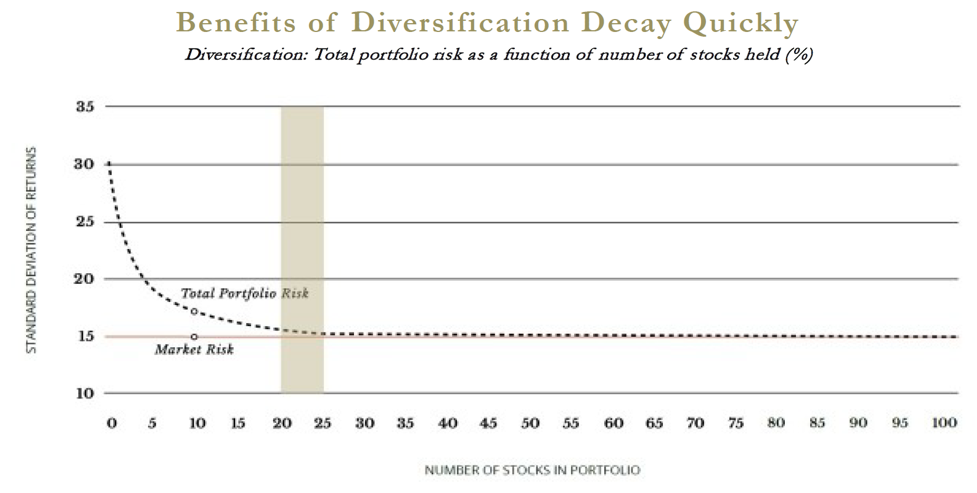

You’re correct, we run a fairly concentrated portfolio, typically holding 20-25 companies. We want our resources focused on the best ideas we have, and we want those ideas to count. Having said that, we also recognize all the work that has shown the “free” benefits of diversification from a risk perspective in the construction of a portfolio. However, that incremental benefit basically becomes de minimis beyond that zone of 20-25 stocks. In his classic book A Random Walk Down Wall Street, Burton Malkiel discussed the benefits of diversification and the diminishing benefit of it beyond 25 stocks in a portfolio. We used that data and created this chart to illustrate his point (Source: Malkiel, Burton Gordon. A Random Walk down Wall Street: The Time-Tested Strategy for Successful Investing. New York: W.W. Norton, 2003. Note: The standard deviation is a statistic that measures the dispersion of data relative to their mean. When applied to the annual rate of return of a portfolio, it describes the historical volatility of returns of that portfolio).

It just so happens 20-25 also corresponds with our own intuition based on experience of the level of concentration that we are comfortable on any single position (3-10% portfolio weight). Our highest weighted positions will be those with the highest convictions crossed with the greatest discounts to our estimate of fair value.

As fundamental investors, we do not consider stock price volatility in our portfolio weighting at all, though we do consider fundamental cyclicality or unpredictability or volatility of cashflows in our fundamental conviction scaling.

Similarly, rebalancing has nothing to do with price performance on its own, but to the extent it impacts thresholds we have on position size vs discount to intrinsic value, that will trigger a rebalancing among certain positions within portfolios.

10. Regarding diversification within the client portfolio, to maintain overall portfolio volatility at a level that fits his or her financial situation and personal outlook. I think this is a great idea. What are the positives and negatives, from your own experience? (I like the idea of the Ulysses pact- is that something you look at doing)

Within the context of our clients’ portfolios, we consider their personal objectives, cash needs, age, and risk tolerance. At that high level we’ll decide with each client what makes sense within the context of these factors as far as mix of equities for long-term growth of capital vs cash needs over the short to medium term. Having their cash needs met in the medium term aligns their cash flow needs with the objectives we jointly agree to for the long term. That long term equity investment portion is then funneled into the equity portfolio strategy we’ve discussed. Studies have shown that the biggest disconnect between clients’ portfolio objectives and actual results happens when they are unable to follow through on a well-thought out investment strategy because their short term needs or fears cause them to take actions that are misaligned with the long term objective and strategy. So we do our best to help them manage through this right from the getgo, by creating a well aligned portfolio structure, while keeping them informed and calm through both exuberant and tumultuous periods in the market.

Additionally, I’d add that our regular communications informing them about the companies they own also helps them understand the value our portfolio companies create, which makes them more tangible investments than a set of tickers with randomly fluctuating prices. Our companies create real value for their customers every day, and that is important to recognize regardless of the meandering price action of their stock price within any shorter-term context. That value creation and the moats our companies build is what underpins our confidence in their longer-term intrinsic value and that is important for our clients to understand in order to build their confidence in sticking with the portfolio. That is as far as we go towards the Ulysses pact!

In the long term, we believe the intrinsic values and stock prices converge, and that is exactly why the alignment of investment objectives, portfolio structure, and client communication is so important!

11. One of my idols when I was young said – every good long-term investment, starts as a good trade…to what extent do you care about trying to time your entry point? Is it just the distance to the target price that matters? Or a target price range, which in any case has a midpoint. You think in terms of confidence intervals & probabilities at all?

We are of the belief that if you do deep enough work and think through the range of probabilities of outcomes for a specific company with a strong moat, you can pick the midpoint and use that as the best gauge of an expected intrinsic value. We use that point estimate as our north star as far as valuing a company.

We have guidelines in place that make it so that we have a balance between a realistic view of how fundamentals could play out with a set of guardrails around our long-term assumptions that build in a reasonable level of conservatism in our valuation. We hope that over time, as fundamentals play out, that the margins of safety we have built in lead to better outcomes generally than our midpoint expectation of possible outcomes.

We don’t really try to time our entry points because we use a disciplined approach to sizing positions based on discounts to fair value and qualitative conviction ratings as we’ve discussed. So, our view is that timing is nothing more than luck rather than a skill we possess in building into a position. We’d rather do the important fundamental work to properly value companies then just let our “automatic” trading system run sizing based on that discount and conviction, however that plays out.

12. When you are wrong, or less right, how do you deal with that? You write like this “However, if our original assessment of a company’s prospects weakens or market prices increase dramatically in the short term, we will adjust our position as necessary”. Fixed signposts? You recently discussed Google in a great way (see below). Maybe an example where you closed a position. Does the stock price matter, i.e. let’s say it starts to weaken, a signal that things are turning or not?

Like any good, rational investor, we incorporate new information into our analysis as quickly as possible, whether positive or negative. And we’ve had our fair share of being wrong on companies in both directions, whether it turned out we exited after a loss or exited too early because we hadn’t understood the full dynamics of growth or profitability.

We don’t use price signals directly for trading per se, but we will reevaluate our thesis on occasions when the price action appears to indicate (positive or negative) that the market is reassessing its view of a stock. We’ll spend some extra time during our “maintenance” period to actively seek out relevant information beyond our normal streams to be sure that we have as accurate a view of the information being ingested by the market that leads to dramatic, unexpected price moves before they trigger a trade to either buy more or sell a portion or all of our position (again based on current conviction and discount/premium to our fair value assessment). More often than not, we find that the market is being driven by something other than our long-term assessment of the company in question and do nothing to change our fair value estimates. However, sometimes we find that there is important new information that changes our opinion on a company’s fundamentals, which then leads to a reassessment of our fair value and position size.

For examples of some of these, please refer to our blog posts where, we’ve discussed many of our positions. The most recent positions where we’ve changed our opinion and exited have been Trupanion (TRUP), explained here, and Apple (AAPL), which we exited after about a decade of ownership because we didn’t think its massive iPhone business could grow much more than a low single digit growth rate going forward after it won the vast majority of its targeted addressable market amidst a mature market and extending replacement cycles. While Apple has created some great adjunct businesses, it will take some time before their scale will offset the slowing iPhone business in our view.

13. Do macro impact your research? I have inserted a quote from your April call below. Do you adjust holdings on the back of a macro view or not? Please elaborate.

“The fact is we are 100% certain that a recession will occur… someday. It is just that neither we nor anyone else knows exactly when. So in thinking about the earnings growth of our portfolio holdings, we focus more on the appropriate growth rate across a full economic cycle that includes a recession while recognizing that the exact timing of that recession is not knowable, but to the extent it becomes more likely to occur sooner rather than later, we will appropriately incorporate this into our company specific forecasts.”

We are bottoms-up fundamental investors, so we don’t generally use short term macro calls as important determinants of our investing strategy. However, changing data will impact our analysis such as changing interest rates for our financial holdings like First Republic Bank (FRC) or Charles Schwab (SCHW), or loads and pricing data on trucking for example in the case of Landstar (LSTR).

Where we do use macro data, is on long-term trends that we think reflect the economic context in which we are assessing a company’s business prospects. Examples of this are long term GDP, inflation, or interest rate trends, population growth, housing demand, internet search trends, digital spending, passenger airline miles, advertising spending, etc. Oftentimes short- or medium-term cyclical variations from the long term underlying trends will lead to a mispricing in the market price of company (positive or negative) relative to our forecast based on a return to trend that will create opportunity for us and we will take advantage of that where it’s applicable.

Occasionally, either the historical trends may see a permanent break due to a fundamental economic, regulatory, or cultural shift, and sometimes we get that right ahead of time, and sometimes we don’t. The future is always uncertain, but history does tend to “rhyme”, so it’s our belief that it is the most rational way to view the world. Fortunately, our focus on a narrow set of companies often results in us not being surprised when such changes do occur.

Thanks very much for taking the time to have this discussion with us Bo, and we hope that it will be useful to your readers. We’re always happy to take feedback and follow up as we continue our investment journey!

Ensemble on Google:

But in allocating their excess capital we have been less enthusiastic. While Google has been criticized in the past for the M&A they engage in, YouTube and DoubleClick are two hugely successful acquisitions with YouTube ranking as one of the smartest acquisitions in the internet age. But Google has now built such a war chest of cash that they clearly have more than they will ever need, and we think shareholders would be better served if the company began to pay a dividend, bought back stock and used more debt in their capital structure to finance more return of capital. We had hoped that Ruth Porat, the CFO they brought in from Morgan Stanley, would be instrumental in improving capital allocation. But after some initial positive signs, it seems that for whatever reason, Porat is no longer focused on making this happen. The other management issue we’re tracking is the company’s relations with their employee base. For pretty much all of their history, Google has been considered one of the very best places to work. They have pioneered much of what we think of as modern Silicon Valley corporate culture with an employee base that has been raving fans of the company. But last year, employee concerns around the company’s work with the military, and issues of gender equality and sexual harassment became flashpoints between management and its employees. Of particular note to us was the various reports on the company paying large severance packages to key senior employees who were forced out after accusations of sexual harassment. In our view, Google management’s handling of these cases has not been good. We believe for the short-term health of their corporate culture and their long-term ability to attract the best and brightest employees, they must do better. By “do better” we mean behave in a way that satisfies their employee base and preserves the belief that Google is one of the best places to work for the smartest, most technically savvy people in the world. To the extent that the company is not able to manage employee relations constructively, our confidence in the long term success of the business would deteriorate and should we decide to exit our position, something we are not currently contemplating, it would be due to our assessment of the long-term health of the business.

{kind=link}